Residential rental market – are we at the bottom?

After a soft couple of years for the rental market nationally, we may have found the floor. As you can see in the graph, the national median rent has stopped declining and has been more-or-less flat for 11 months now.

Demand is growing with migration showing signs of a recovery. The net gain for the March 2026 year was 24,200, up 73% on the year before, driven mostly by fewer departures. Trade Me search data shows a 12% year-on-year increase in tenants searching for properties in Auckland.

Auckland’s median rental price is $660 and has been for 5 months. Trade Me is saying that rental supply is down by 9% – however that is only measuring new listings to the site. Supply is actually still increasing with a 12.6% increase in total number of properties available in Auckland today, compared to the last time we did a market update in March (up from 5,263 to 5,894).

So, what does this all mean? Rents seem to have stabilised, so in most cases if your annual rent review was due today, the advice would be to keep your rent as it is. It makes sense that rents are flat with both demand and supply increasing at a similar rate; we need either supply to drop or demand to increase even more to see any rise in rental prices.

Regional picture

Auckland and Bay of Plenty now share the title of most expensive region, both sitting at $660 per week in May. Canterbury is the standout performer, up 1.8% year on year to $580. Otago sits at $640, Hawke’s Bay at $620, Waikato at $595, and Southland remains the most affordable at $500. Wellington has had the toughest run of the major centres: the median is now $600, down $20 on a year ago, and the government’s target of around 8,700 fewer public service jobs by mid-2029 is likely to extend that pressure.

Interest rates

The OCR was held at 2.25% through April and May, but the Reserve Bank just lifted it 25 points to 2.50%, the first increase since May 2023. The move was widely anticipated, and the Bank says further increases are likely at upcoming meetings (next reviews 2 September and 28 October).

The inflation picture has improved. The RBNZ now expects inflation peaked at 3.9% in the June quarter, easing back to the 2% target by mid-2027, a softer path than the 4.3% peak forecast just weeks ago.

Some perspective: even at the 3% ANZ and Westpac are picking for the end of 2026, the OCR would still be historically low, and average mortgage rates around 5% are a far cry from the 7%-plus that squeezed investors through 2023 and 2024. 2026 is also an election year, with capital gains tax, interest deductibility and wider property tax settings set to become campaign talking points. Contact Sam Hewetson with any questions about buying or selling.

The housing market – prices easing into winter

The sales market has softened heading into winter. The national average asking price on Trade Me fell to $833,800 in May, down $50,000 (5.7%) over the three months since February’s two-year high, with Auckland dropping just over $91,000. Eleven of fifteen regions recorded falls in May, and a large overhang of unsold stock suggests buyers will hold the upper hand for a while yet. With rates still low and prices coming back, it’s a window worth watching for anyone weighing up their next purchase.

What’s happening at Aspire?

We’re thrilled to be named one of the Top 8 Property Management Companies by Trade Me.

Our MD Mike Atkinson was back on the OneRoof radio show on ZB, this time talking about the rental market compared to household income. Have a listen here.

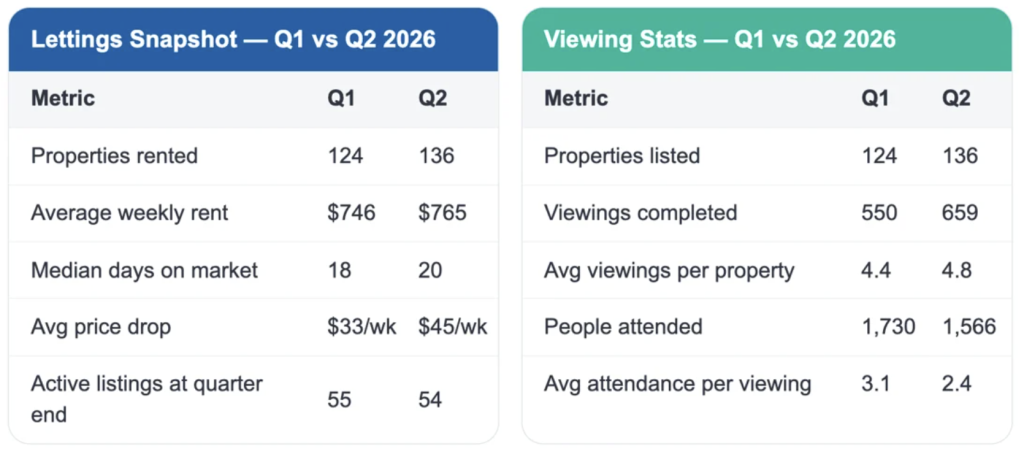

Q2 usually brings a seasonal dip in tenant demand, but this quarter we actually rented more properties than in Q1. That said, the winter pattern is showing through: fewer tenants at each viewing, properties taking slightly longer to rent, and some needing a bigger price adjustment to get across the line. With lease renewals clustering around summer, Q2 and Q3 are always the more challenging quarters to find tenants.

Expanding our staff and portfolio

Our team has expanded to 32 staff – we welcome Joy Du and Katrina Li – both fluent in Mandarin and English, so if you prefer to converse in Mandarin, feel free to reach out to either of them, or Maggie Du, all who will be happy to help you.

Also on staff we have Chris Jablonski, who is fluent in Polish, Vishal Sharma, who is fluent in both Hindi and Nepali and Joyce who is fluent in Cantonese.

You’ll find their contact details on the about us page, don’t hesitate to reach out if you’d like to speak to any of them.

We now manage 1,219 residential and commercial properties across Auckland, Waikato and Bay of Plenty. On the commercial side, we added Castaways Resort to the portfolio this quarter, along with tenanted retail blocks and office space.

Aspire Intelligence – our AI portal and tools

We’ve rolled out three new tools over the past quarter that are already making a real difference. Daryl, our AI Digital Property Manager, helps us respond to rental enquiries faster than ever, with personalised, human-approved replies sent within 15 minutes of an enquiry arriving, day or night, so our properties never lose a good tenant to a slow response.

Our new Maintenance Deep Research tool gives us a complete AI-assisted analysis of any property’s maintenance history in about a minute, spotting recurring issues, checking contractor value for money and flagging anything unusual, which means better answers for our customers and smarter decisions about our properties. And every contractor invoice now goes through AI scanning that acts as a second pair of eyes on all transactions, checking bills against the original job request and flagging scope changes, safety issues and compliance gaps before anything reaches our owners’ statements. Together these tools mean faster tenant responses, fewer surprises and more transparency on every dollar spent at our properties.

Watch how we’re using AI and automation to deliver better results.

Commercial market update – by Lauren and Blake

Retail is stabilising, with demand returning in Auckland led by rising CBD foot traffic and solid regional centres, though Wellington remains soft. Rents and yields are broadly stable. The watch-point is the household budget, with the oil shock pushing inflation higher and consumer spending under pressure.

Office remains the softest sector, split sharply by quality. Prime Auckland CBD vacancy has edged up to around 8.5%, mostly reflecting new premium buildings and tenants trading up, while the real pressure sits in secondary space, where incentives keep rising and tenants hold the leverage.

Industrial is still the tightest sector but past its peak, with vacancy at 2.8%, a decade high but low by any historical measure. Enquiry is strongest for prime South Auckland stock, yields around 5.6% are stable, and a measured development pipeline keeps oversupply risk contained.

Make the move to Aspire today!

If you like the sound of how we operate, join us today! With over 700 genuine reviews on Google and a 4.9 rating, you know you’ll be in good hands.